The Continuity Index: A Framework for Measuring Whether Saudi Family Institutions Survive Their Founders

The Continuity Index proposes a new framework for measuring whether Saudi family businesses are prepared to survive beyond their founders, focusing on leadership, governance, reputation, institutionalization, and succession.

Most Saudi institutions are designed for growth, while few are meant to endure. The Continuity Index evaluates the underlying structure that shapes an enterprise’s future.

Strategic Essay | Prince Researcher

Abstract

Every Saudi founder believes their institution will outlast them. Few can explain how. Family enterprises account for close to 60 percent of private sector GDP contribution in the Kingdom, yet a single inherited statistic has shaped global thinking about their survival odds for nearly 40 years. That statistic is widely misquoted. The original research found something narrower and more forgiving than the version now repeated in consulting brochures worldwide. The deeper pattern, supported by Saudi-specific governance research, points elsewhere. Institutions rarely fail due to weak business models. They fail from missing architecture: undefined decision rights, undocumented knowledge, and reputational risk left unmanaged. This essay proposes the Continuity Index as one response to that gap, a framework that scores institutional readiness across five dimensions: Leadership, Governance, Reputation, Institutionalization, and Succession. Each dimension is assessed against a defined set of indicators and produces its own score, forming a readiness profile rather than a single composite number. The framework does not predict survival. It is also new, built through advisory practice rather than decades of longitudinal study, and its value will depend on testing across real institutions. The central argument is simple. Legacy is not inherited. It is engineered.

Introduction

Saudi Arabia's private sector rests on family enterprise. Grant Thornton estimates that family-owned businesses account for close to 60 percent of the private sector's GDP contribution, spanning retail, construction, manufacturing, finance, and hospitality. A separate estimate from the National Center for Family Business puts family enterprises at close to 95 percent of private sector entities by count, a different measure of how many businesses are family-owned rather than how much economic output they generate, and the two figures should not be conflated. The founders who built these companies, mostly between the 1960s and the 1980s, are now in their seventies and eighties. Their successors were educated abroad and came of age in a different country than the one their grandparents built.

This is not a crisis of capability. It is a structural condition. The Kingdom has named it directly. INSEAD researchers describe the current period as Saudi Arabia’s "succession decades," the stretch of years in which the founding generation of the modern private sector hands control to heirs with different instincts, different risk tolerance, and a different daily relationship to the business itself.

Governments have responded with infrastructure, not just awareness campaigns. The Kingdom established the National Center for Family Business by royal decree, a joint initiative between the Ministry of Commerce and the Federation of Saudi Chambers. Public sources differ on the exact founding date, with KPMG Saudi Arabia citing 2012 and other industry sources citing 2014, a small but telling reminder that even institutional facts in a fast-moving private sector are not always settled at the source. Vision 2030 has accelerated reforms to the Companies Law, succession-related licensing, and family business professionalization programs. The bet, in effect, is that institutions can be built faster than founders retire.

What is missing is not awareness. It is a measurement. Founders know continuity matters. Few have a precise way to assess how close their own institution is to surviving them. This essay traces the origins of the popular fear of family business failure, examines the academic model that explains the problem without measuring it, and proposes a framework designed to close that gap for Saudi institutions specifically.

Theoretical Framework

Four academic lenses explain why family institutions succeed or fail. Each lens alone is insufficient.

Organizational theory treats institutionalization as the process by which informal practice becomes formal structure. A business institutionalizes when its knowledge, culture, and operating logic no longer depend on any single individual. Saudi family enterprises often skip this step. A founder’s twenty years of personal supplier relationships function as a genuine asset, but one that cannot be inherited. It can only be transferred by design, and only if the transfer begins years before it becomes urgent.

Sociological theory of capital, drawing on Bourdieu, explains why reputation belongs inside a continuity framework rather than outside it. In a Gulf context, a family’s name functions as social capital, accumulated across generations of visible conduct and public trust. The empirical case for this connection has gotten considerably stronger in recent years. A 2025 meta-analysis pooling 85 studies and more than 152,000 observations found that corporate social responsibility practices improve family firm performance, with the strongest effects evident in long-term sustainability rather than short-term profits. A separate study of firms during the 2008 to 2009 financial crisis found that those with higher social capital, measured through community and stakeholder trust, posted stock returns four to seven percentage points higher than less-trusted peers during the crisis itself, with the advantage persisting through the recovery that followed. Research focused specifically on Gulf family enterprises has found a related pattern: family involvement is linked to firm reputation, and reputation, in turn, partly mediates stakeholders' perceptions of financial performance. Reputation, in other words, is not a soft variable sitting beside the hard ones. It behaves like an asset, one that pays out most visibly in the moments an institution can least afford to be untested.

Family business economics, including agency theory applied to closely held firms, explains the conflict beneath succession disputes. When ownership, management, and family identity overlap within the same set of people, decision rights are inherently ambiguous. Conflicts over authority, financial return, and informal promises are rarely legal disputes at their root. They are structural disputes, arising from roles that were never written down.

Socioemotional wealth theory explains why family owners often prioritize non-financial goals over financial ones. The framework distinguishes between the social and emotional components of this wealth, a family’s public standing on one hand and the emotional bonds tying members to the enterprise on the other, and treats both as core properties that owners actively protect through their decisions, sometimes at a measurable cost to short-term return. This is the clearest theoretical explanation for why reputation cannot be treated as a soft variable inside a continuity framework. It is one of the things family owners are most motivated to defend, which is exactly why it behaves like an asset rather than a courtesy.

Each lens illuminates part of the mechanism. None of them, alone, produces something a founder can act on. That requires moving from explanation to measurement.

Case Studies

The National Center for Family Business: Building Infrastructure Before the Crisis Arrives

Before the center existed, Saudi family business disputes had no dedicated institutional home. Conflicts over succession, governance, and inheritance were handled informally, through family negotiation or, when that failed, through courts not designed for the relational complexity of family enterprise.

The Kingdom built something specific. A royal decree established the National Center for Family Business as a joint initiative between the Ministry of Commerce and the Federation of Saudi Chambers. Its mandate is consistent across sources: research, governance, conflict resolution, and reform of the Companies Law. INSEAD researchers note that the center also trains and licenses mediators in partnership with the Ministry of Justice, under an approach described as preventive justice, an attempt to resolve disputes before they harden into litigation.

In remarks reported by Argaam, NCFB's chief executive described the center resolving approximately ten family business disputes in a recent period through advisory sessions, proposed solutions, and consensus-building. The center also developed a formal guide for preparing family charters with the Ministry of Commerce, and cooperates with the Ministry of Justice's digital platform for dispute resolution.

NCFB's own survey work points to why this is urgent. Roughly 60 percent of Saudi family enterprises do not have a documented succession plan, and a comparable share have no clear blueprint for how ownership or management will actually transfer when the time comes. That gap is not a footnote. It is the condition the center was built to address.

This reveals something the global statistics miss. Saudi Arabia did not wait for a generation of family businesses to fail before building infrastructure. It built that infrastructure during the successive decades itself, treating continuity as a national institutional priority rather than a private family matter.

The Survival Statistic: How a 1987 Study Became a Permanent Anxiety

Before the Continuity Index, the dominant data point in family business literature was a single number. Thirty percent of family businesses survive to the second generation, thirteen percent to the third, and three percent to the fourth. It appears in consulting brochures and government white papers worldwide, almost always uncited.

The number traces to a 1987 study by scholar John Ward of Northwestern University’s Kellogg School, published in his book Keeping the Family Business Healthy. His team examined 200 Illinois manufacturing companies that existed in 1924, tracking their fates through 1984, a period that includes the Great Depression. Twenty percent of those firms still survived as independent companies under their original name, and of that group, thirteen percent remained family-owned. Ward’s own writing described this as roughly a third of firms lasting through the second generation, a sixty-year span, not to mention.

What happened afterward is well documented in the family business literature itself. A 2023 review by Family Business Magazine traces how the word “through” was repeatedly misquoted as “to,” a substitution that understates real firm longevity by decades. The Family Business Consulting Group, the firm Ward co-founded, has separately acknowledged the same distortion, along with a second one: the original study counted a firm as a failure if it was sold, merged, or transitioned to employee ownership, regardless of whether that outcome was a success by any other measure.

This reveals the problem the Continuity Index was built to address. A statistic copied from one era, one industry, and one region tells a Saudi enterprise founded in 1975 almost nothing about its own risk. It produces a mood of dread, not a diagnosis. Mood is not actionable. A measured gap in succession readiness is.

The Three-Circle Model: A Map Without a Gauge

Before the Continuity Index, family business research already had a foundational framework. Harvard Business School’s Renato Tagiuri and John Davis developed the Three-Circle Model in the late 1970s and formally published it in 1996. It maps a family enterprise as three overlapping circles: family, business, and ownership. Anyone connected to the enterprise sits somewhere in the overlap.

The model’s contribution was making visible something that earlier two-circle frameworks had missed. Ownership creates its own distinct set of interests, separate from family loyalty and separate from operational management. Since then, nearly five decades of family business research have tested and refined it.

What the model does not do, by design, is measure anything. It explains why a shareholder cousin who is not an employee feels excluded from decisions. It cannot tell the family whether their succession readiness this year is better or worse than it was two years ago.

This reveals the specific gap this framework attempts to address. Not a replacement for the Three-Circle Model, but an attempt to operationalize the questions it raises into something a Saudi institution can score, track, and act on over time.

Synthesis Framework: The Continuity Index

The Continuity Index is a proposed framework for measuring institutional readiness across five dimensions: Leadership, Governance, Reputation, Institutionalization, and Succession. Each dimension answers a question the founding generation rarely asks aloud, because asking it means admitting that survival is not guaranteed by effort alone.

Leadership asks whether the next generation of decision-makers exists and is ready. It is measured through successor identification, leadership pipeline depth, and demonstrated capability under real pressure, rather than ceremonial titles. A family business can have an heir without having a leader. The two are frequently confused, and the confusion is expensive. Saudi research on succession practices documents a specific version of this mistake: suddenly placing a son or daughter in a leadership role, without prior preparation, to test their capabilities under pressure. The practice tends to backfire, eroding both the individual’s confidence and the organization’s trust in the new leadership, which is exactly what gradual, training-based succession is designed to prevent.

Governance asks whether decisions move through structure or through proximity to the founder. This dimension examines board effectiveness, the existence of a family council, and whether decision rights are written down or simply assumed. Saudi-specific research consistently identifies the family charter as one of the highest-leverage interventions available, because it converts implicit assumptions into explicit agreements before a crisis tests them. The same research flags a related risk worth watching directly: choosing leaders based on closeness to the founder rather than demonstrated competence, a pattern linked to both weaker institutional performance and a sense of unfairness among family members who were passed over. Governance structures that score well on this dimension typically separate ownership from executive management and keep ownership concentrated among direct family members rather than spouses, both of which reduce the number of competing interests the system has to manage.

Reputation asks how durable the institution’s standing is, independent of any single person inside it. Most consulting frameworks omit this dimension entirely. That omission reflects a narrower definition of continuity, inherited from Western governance literature built for publicly listed companies, where ownership and identity are legally separable from any family name. That separation does not hold in the same way in a Gulf context, where research has repeatedly linked family reputation to firm-level performance and to access to capital and talent, and where firms with stronger social capital have been shown to outperform less-trusted peers, particularly during periods of crisis. Governance protects an institution internally. Reputation protects it externally. A framework that measures one without the other measures half the risk.

Institutionalization asks whether the knowledge, culture, and operating systems that make the enterprise work reside in documented processes or only in the founder’s head. This dimension is the least visible from the outside and the most catastrophic when absent.

Succession asks whether the handover of control has a designed sequence, defined contingency triggers, and clarity on ownership transfer. A successor can be fully capable, and a transition can still fail, because no one has defined when it activates or what happens if it must activate earlier than planned.

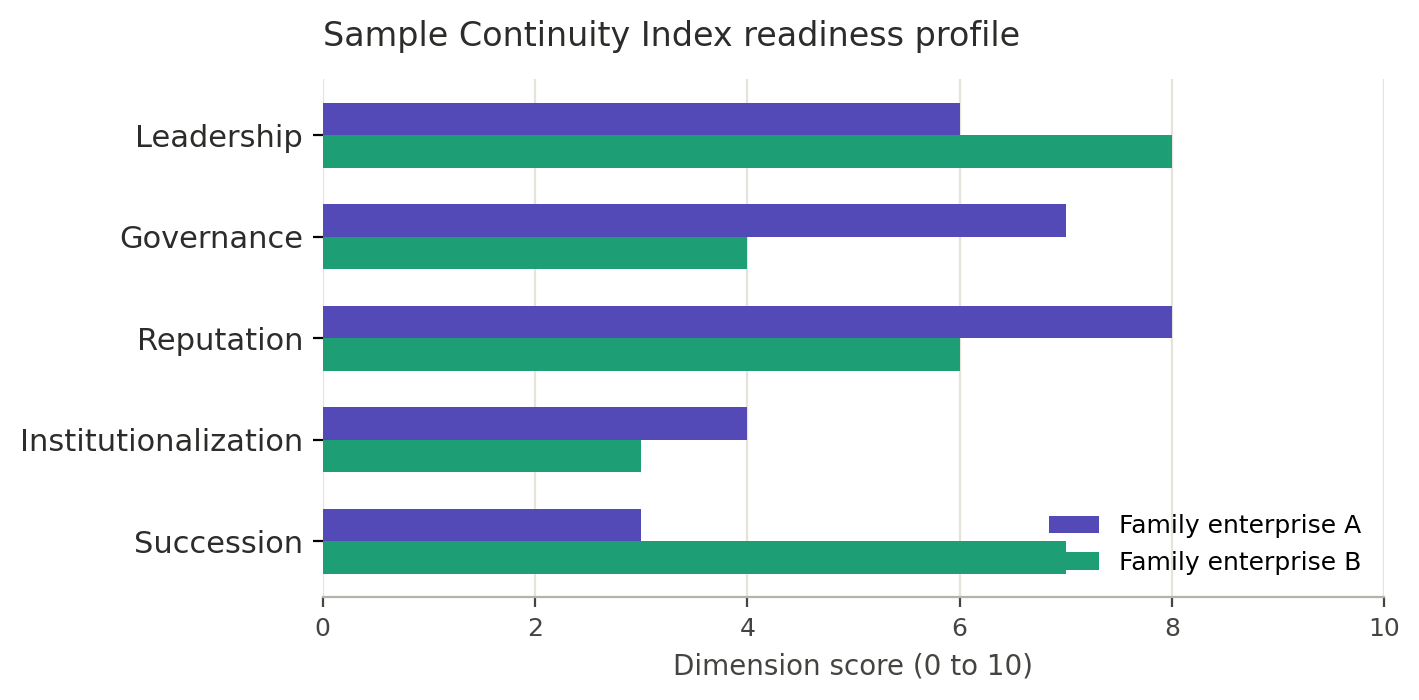

The figure below sets out the five dimensions and the kind of output the Index produces.

How the Index Is Scored

A score is only useful if it is built on something more specific than impression. Each of the five dimensions is assessed against a defined set of indicators rather than a single survey question. Leadership is evaluated through successor identification, demonstrated decision-making under real pressure, and the depth of the leadership pipeline beyond the immediate successor, with structured, gradual preparation weighted favourably against sudden or untested leadership placements. Governance is evaluated through the existence and activity of a board or family council, the presence of a written family charter, and the clarity of decision rights across family, ownership, and management roles, including whether leadership selection follows demonstrated competence rather than closeness to the founder. Reputation is evaluated through documented standing with key external stakeholders, the presence or absence of unresolved public disputes, and the institution's track record during periods of visible uncertainty. Institutionalization is evaluated by how much operating knowledge, supplier relationships, and culture are documented rather than kept only in the founder’s head. Succession is evaluated through the existence of a written succession plan, defined trigger conditions for transition, and pre-agreed ownership transfer mechanics.

Each dimension is scored independently, typically on a ten-point scale, based on structured interviews, a review of existing governance documents, and observed practice rather than self-report alone. The five scores are not averaged into a single number. They form a profile. A family enterprise can be governance-strong and succession-weak. Another can have a highly capable next generation and almost no documented institutional knowledge. Collapsing five distinct risks into a single composite figure would make the Index easier to market but considerably less useful to act on. The sample profile below illustrates the kind of comparison this produces: two hypothetical enterprises with different risk concentrations across the same five dimensions.

How the Assessment Works in Practice

An assessment is most useful at three points: early, while the founder is still active and the cost of change is low; in the years immediately before a planned leadership transition; and on a recurring basis afterward, typically every two to three years, to track whether earlier gaps are closing or widening. A single score, taken once, is a snapshot. A score tracked over time becomes evidence of whether the work being done is actually closing the gap.

Participation matters as much as timing. A credible assessment draws on structured interviews with family members across different generations and roles, not only the founder or the designated successor, alongside key non-family executives who can speak to how decisions are actually made day-to-day. An external facilitator, typically a family business advisor, is usually necessary to surface disagreements that family members are reluctant to raise with each other directly.

The results are diagnostic, not prescriptive. A low score in Institutionalization does not tell a family what to do. It tells them where to look. The actual work, documenting operating knowledge, building a leadership pipeline, formalizing a family charter, designing a reputation strategy that survives leadership change, is advisory work, relationship work, and often slow work. The Index cannot do that work. It can make it clear that the work is needed, and roughly where to start.

What the Index Cannot Do

Intellectual honesty requires stating the limits plainly. The Continuity Index cannot resolve a family dispute that has already hardened into personal grievance. It cannot manufacture a willing, capable successor where none exists. It cannot substitute for legal structuring, tax planning, or the kind of slow trust-building that no framework, however well designed, can compress into a quarter.

It is also, by definition, a young framework, built through advisory practice rather than decades of longitudinal academic study, in contrast to a model like Tagiuri and Davis’s, which has been tested and refined across nearly five decades of family business research worldwide. The five dimensions proposed here reflect a synthesis of existing governance, succession, and institutional trust literature, adapted to the realities of Saudi and Gulf family enterprises, rather than a claim to have discovered something entirely unprecedented. The framework has not yet been tested on a meaningful sample of Saudi family enterprises, and the indicators described above should be read as a starting point for design rather than a finished instrument. Its value, if it has any, will be proven the way any applied framework earns credibility: through use, revision, and the honest reporting of where it was wrong. Future work in this area will apply the Index to specific cases and report what the scoring gets right and where it needs to change.

Conclusion

The founding generation of Saudi Arabia’s modern private sector did something rare. They converted personal risk into institutional scale, often within a single working lifetime, often without a roadmap. That instinct cannot be inherited by the next generation. What can be inherited is structure.

The Continuity Index is one attempt to name what that structure looks like. It scores five dimensions a founder can measure, rather than merely hope for: Leadership, Governance, Reputation, Institutionalization, and Succession. It does not guarantee survival. No framework does. It offers something more modest. A way to see, early and clearly, whether the institution being built today ends with its founder or begins there.

For founders and family councils reading this, the practical next step is straightforward. Run a baseline assessment across all five dimensions before the next leadership transition, not just a succession plan in isolation. A succession plan built on top of weak governance or undocumented institutional knowledge is a plan built on sand, however carefully the handover date is chosen.

Saudi Arabia is living through its succession decades now, not as an abstraction but as thousands of concurrent transitions inside thousands of family enterprises. The institutions that treat this as a measurable discipline, rather than a private anxiety, will be the ones still standing when the next transition arrives.

Legacy is not what a founder leaves behind. Legacy is what continues without them.

References and Further Reading

Academic

Bourdieu, P. (1986). The Forms of Capital. In Handbook of Theory and Research for the Sociology of Education.

Chen, W., Zhou, A. J., Zhou, S. S., Hofman, P. S., and Yang, X. (2022). Deconstructing Socioemotional Wealth: Social Wealth and Emotional Wealth as Core Properties of Family Firms. Management and Organization Review, 18(2), 223–250.

Combs, J. G., Jaskiewicz, P., Ravi, R., and Walls, J. L. (2023). More Bang for Their Buck: Why (and When) Family Firms Better Leverage Corporate Social Responsibility. Journal of Management, 49(3).

Lins, K. V., Servaes, H., and Tamayo, A. (2017). Social Capital, Trust, and Firm Performance: The Value of Corporate Social Responsibility During the Financial Crisis. Journal of Finance, 72(4), 1785–1824.

Oduro, S., et al. (2025). Corporate Social Responsibility and Family Firm Performance: A Meta-Analytic Review. Corporate Social Responsibility and Environmental Management.

Tagiuri, R., and Davis, J. A. (1996). Bivalent Attributes of the Family Firm. Family Business Review, 9(2).

Ward, J. L. (1987). Keeping the Family Business Healthy: How to Plan for Continuing Growth, Profitability, and Family Leadership. Jossey-Bass.

Zellweger, T. M., Nason, R. S., and Nordqvist, M. (2011). From Longevity of Firms to Transgenerational Entrepreneurship of Families: Introducing Family Entrepreneurial Orientation. Family Business Review.

Academy of Strategic Management Journal (2020). Family Businesses (FBS) in Gulf Cooperation Council (GCC): Review and Strategic Insights.

Institutional and Industry

Grant Thornton Saudi Arabia. Family Businesses in Saudi Arabia: The Secret to Long-Term Success.

KPMG Saudi Arabia (2023). Succession Planning in Family Businesses. Joint research with the National Center for Family Business, led by Dr. Hanoof Abokhodair and Dr. Dalal Alrubaishi.

KPMG Saudi Arabia. Conflict Resolution.

National Center for Family Business (NCFB). Public statements via Argaam (2024).

National Center for Family Businesses and Riyadah Center, Dr. Bandar Al-Amer. From Generation to Generation: Family Giving and Family Enterprise Sustainability.

INSEAD Knowledge (2025). Saudi Arabia Tackles the "Succession Decades."

Takmil. Family Business Governance in Saudi Arabia.

Family Business Magazine (2023). A Critical Look at "Survival" Statistics.

The Family Business Consulting Group. Family Business Survival: Understanding the Statistics.

Center for Family Business, Case Western Reserve University. FAQ.

Journalism

Arab News. Saudi Arabia's New Corporate Law Supports Family Firms, SME Investments.

© Strategic Essay — Prince Researcher | For Academic and Editorial Use